.png)

What is Discount for Lack of Marketability (DLOM)?

Privately held companies are significantly less liquid than their publicly traded counterparts, meaning their shares are more difficult to sell.

The Discount for Lack of Marketability (DLOM) is used in company valuation to adjust for this lack of liquidity, making the shares in a private company worth less than they would be in a public company.

Why DLOM matters in valuations

When valuing a private company, investors often assess its potential to generate future cash flows and use the Discounted Cash Flow (DCF) method to estimate its present value.

But that’s only part of the picture.

You also need to consider:

- How easily the company or its shares can be sold

- Whether there’s an active market for those shares

- How long it might take for an investor to realize that value

This is where the Discount for Lack of Marketability (DLOM) comes into play. It adjusts the valuation to reflect the challenges of selling private company shares.

What is ‘marketability’?

Marketability refers to how easily an asset can be sold in the open market at a fair price.

An asset is considered highly marketable if there is a ready market for it, meaning there are many buyers and sellers available.

For example, a stock in a public company like Apple is highly marketable because it can be quickly bought or sold on the stock exchange, with plenty of buyers and sellers available at any time.

In contrast, shares in a private company are not easily marketable, as finding a buyer can be difficult, and even if one is found, they’ll likely expect a discount.

Marketability is closely related to liquidity, but they’re not the same.

Liquidity refers to how quickly and easily an asset can be converted into cash without significantly impacting its price.

Marketability, on the other hand, reflects how easily an asset can be bought or sold in the market.

In other words, marketability speaks to the presence of a market, while liquidity speaks to the ease and efficiency of converting the asset into cash.

How to calculate the Discount for Lack of Marketability (DLOM) using the Mandelbaum factors?

The Mandelbaum factors provide a qualitative framework for estimating the DLOM on private company shares. Rather than relying on a fixed formula, this approach considers ten key factors to assess how marketable the shares are.

The ten Mandelbaum factors include:

- Comparison between the value of a company’s privately held shares and the value of similar publicly traded shares

- Review of the company’s financial health

- Evaluation of the company’s ability to pay dividends and its historical track record of doing so.

- Assessment of the business’s background, industry position, and future growth prospects.

- Quality of the company’s leadership and executive team.

- Level of influence or control associated with the ownership stake being valued.

- Any limitations or restrictions that prevent the shares from being freely transferred.

- Expected holding period required before an investor can sell.

- The company's policies to repurchase or redeem its shares.

- Estimated expenses involved in taking the company public.

How to calculate the Discount for Lack of Marketability (DLOM)?

While the Mandelbaum factors are qualitative, the following methods are quantitative approaches to evaluating the DLOM:

1. Restricted stock method

The restricted stock method estimates the DLOM by comparing the price of restricted shares in publicly traded companies to their freely traded shares in the same company. Restricted shares cannot be sold immediately in the open market, but they are otherwise identical to the company’s publicly traded shares.

The price difference between these two types of shares reflects the impact of illiquidity.

This provides a benchmark for how much less investors are willing to pay for shares that cannot be easily sold.

On average, studies of restricted stock suggest a DLOM in the range of 20% to 35%. However, in some cases, these studies have observed discounts as high as 90%.

This wide variation highlights the importance of considering company-specific factors when determining the appropriate discount.

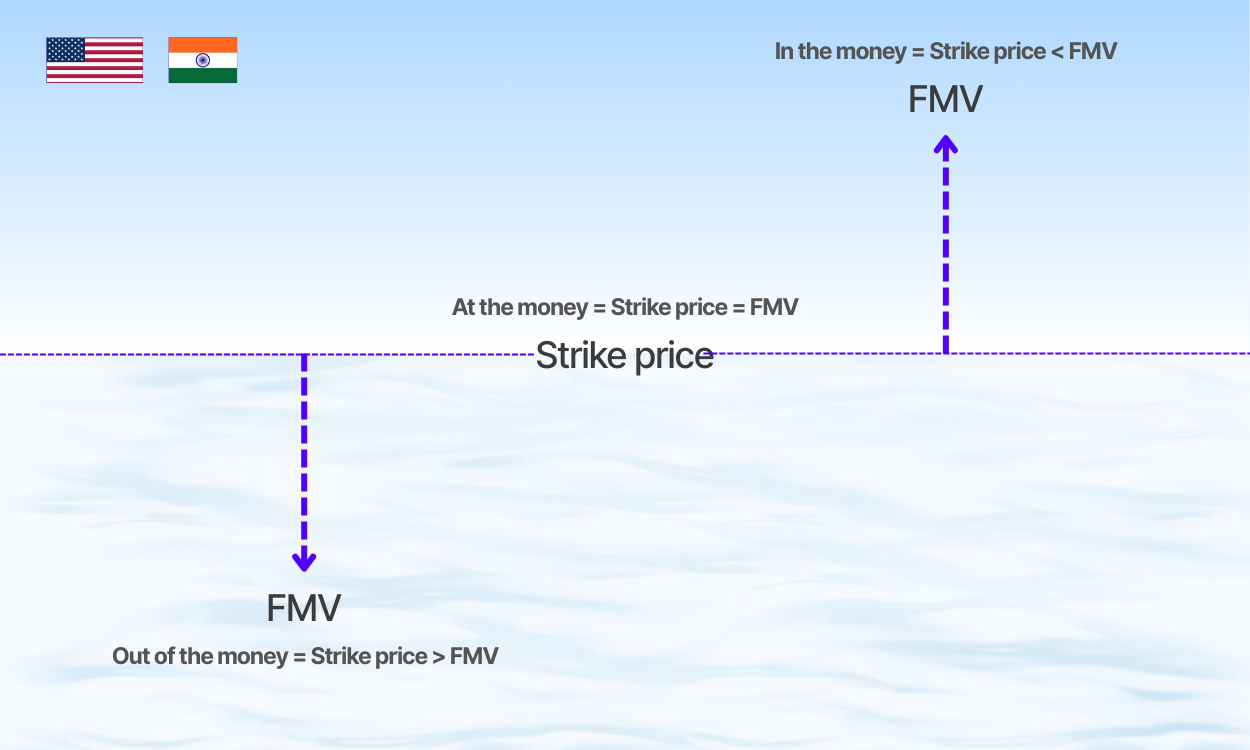

2. Option pricing method

The option pricing method uses the value of options to estimate DLOM. The difference between the strike price and the market price of the stock helps calculate the discount.

For example: Let’s say options give someone the right to buy a share for $10, and the actual share is worth $15. The $5 difference can reflect the cost (or discount) of not being able to sell shares freely.

3. IPO method

The IPO method compares the price of a company’s shares before and after its Initial Public Offering (IPO). The difference in value between pre-IPO and post-IPO shares helps estimate the DLOM.

Although private companies don’t have publicly traded shares, the IPO method like the restricted stock method uses data from public markets as a proxy to benchmark marketability discounts for private company valuations.

Studies of pre-IPO typically suggest a DLOM in the range of 40% to 60%.

Challenges in determining Discount for Lack of Marketability (DLOM)

One of the biggest challenges in valuing private companies is the lack of information on the value of their assets. Additionally, tax complications often arise when dealing with ownership interests that are both non-marketable and non-controlling.

All of this makes the valuation process time-consuming, costly, and uncertain.

DLOM, DLOC and DLOL

In the case of a closely held private company with only a few shareholders, giving up ownership can lead to significant financial tradeoffs.

This introduces additional discounts that often overlap with the Discount for Lack of Marketability (DLOM), such as:

Discount for Lack of Control (DLOC): This discount reflects the reduced value of shares that do not offer control over the company’s decisions. For example, a 10% stake without voting rights is usually worth less than 10% stake with voting privileges.

Discount for Lack of Liquidity (DLOL): This discount compensates for the lack of assets that can be converted to cash without significant loss of principal.

Both DLOC and DLOL intersect with DLOM but target different aspects of valuation.

Together, they create a more comprehensive valuation framework for privately held companies.

DLOM vs DLOC

DLOM accounts for the illiquidity of private company shares, focusing on how easily shares can be sold.

DLOC relates to the lack of control over the company that comes with owning a minority stake. Shares without control are less valuable than those that provide control over the company’s decisions.

Both discounts are applied together to provide a comprehensive valuation, but they should not be confused with one another.

DLOM vs DLOL

DLOM focuses on the difficulty of selling an asset due to the absence of a public market. The lack of a ready market for these shares means the owner must accept a lower price to sell them.

DLOL, on the other hand, is concerned with the ability to convert an asset into cash quickly without significant loss of value.

The primary distinction between DLOM and DLOL is that DLOM focuses on the marketability of the asset (i.e., how easy it is to sell), while DLOL focuses on the liquidity of the asset (i.e., how quickly it can be converted to cash without significant loss in value).