In India, Employee Stock Option Plans (ESOPs) are becoming increasingly popular, fueled by the recent IPO boom. The market achieved a significant milestone, raising $12.2 billion in 2024 compared to $6.4 billion in 2023, according to a Global Data report.

However, implementing Employee Stock Option Schemes (ESOS)/ Employee Stock Option Plans (ESOPs) requires thoughtful planning and strict compliance.

What are Employee Stock Option Plans (ESOPs)?

An Employee Stock Option Plan (ESOP) is a benefit plan that provides employees with an opportunity to gain ownership in the company.

It gives them the option to purchase company shares at a discounted price in the future.

This aligns employees' interests with those of the organization.

Who is eligible for ESOPs?

The following individuals are eligible for ESOPs in both listed and unlisted companies:

- Full-time Indian and foreign employees employed by the company, either in holding or subsidiary companies.

- Full-time and part-time directors of the company, excluding independent directors.

Companies issuing shares or stock options to foreign employees must comply with the Foreign Direct Investment (FDI) policy.

Prior approval from the RBI is required if:

- Shares are issued to employees in countries not covered under India’s automatic route for FDI.

- The issuance exceeds sectoral caps or contravenes FEMA norms.

A company cannot issue ESOPs to:

- Independent directors, promoters, and employees belonging to the promoter group.

- A director owning over 10% of the company’s total equity shares, whether directly, through a business entity, or through a relative.

Note: These conditions don't apply to startups under the "Startup India Initiative" for 10 years from incorporation.

A startup is a company with an annual turnover under ₹100 crore with a focus on innovation, intellectual property, and the development of new products with significant potential for creating jobs.

ESOP guidelines and regulations

Employee stock option schemes (ESOS) for both listed and unlisted companies in India are governed by the Companies Act, 2013.

This Act provides a comprehensive regulatory framework that works alongside specific regulations, such as the SEBI (Share Based Employee Benefit & Sweat Equity) Regulations, 2021, which apply to listed companies.

For unlisted companies, the Companies (Share Capital and Debentures) Rules, 2014, are applicable instead of the SEBI regulations.

Setting up ESOP: Direct route vs trust route

There are two ways companies can decide to issue stock options:

1. Direct route: The direct route, often used by unlisted companies, involves the company issuing shares directly to employees upon the exercise of their stock options.

This method is simpler to implement and administer since it doesn't involve an intermediary. The company retains control of the shares and provides them directly to employees when they exercise their options.

2. Trust route: In this method, an ESOP trust is established to acquire and hold the company's shares, which are then allocated to employees over time as they exercise their options.

A trust is typically preferred by large listed companies to manage large-scale ESOPs and ensure liquidity.

If a trust acquires shares in the secondary market, the acquisition limit is 2% of the paid-up equity capital per financial year, with an overall cap of 5% of the paid-up equity capital at any given time.

However, if the trust acquires shares directly from the company, there is no limit on the acquisition.

How to structure an Employee Stock Option Scheme (ESOS)?

Section 62(1)(b) of the Companies Act, 2013, and Rule 12 of the Companies (Share Capital and Debentures) Rules, 2014, lay out the rules for issuing Employee Stock Option Plans (ESOPs) for unlisted companies.

The process for issuing ESOPs under these rules is similar to the one followed by listed companies, as set by the Securities and Exchange Board of India (SEBI).

It includes the following steps:

Step 1: Draft the ESOP scheme

The first step is to draft the scheme, which should clearly outline the key terms like eligibility criteria, vesting schedule, exercise price, and the total number of options to be granted.

Step 2: Secure board and shareholder approvals

Once the scheme is drafted, it requires approval from the board of directors and shareholders.

For both listed and unlisted companies, a special resolution is typically needed to approve the employee stock option scheme.

Step 3: File necessary forms with the Registrar of Companies (RoC)

For both listed and unlisted companies, filing certain forms like MGT-14 with the RoC is necessary for regulatory compliance.

For listed companies, additional disclosures to the stock exchange may also be required.

After obtaining the necessary approvals and completing the paperwork, the company can implement the scheme.

How to allot ESOPs to employees

1. Vesting period

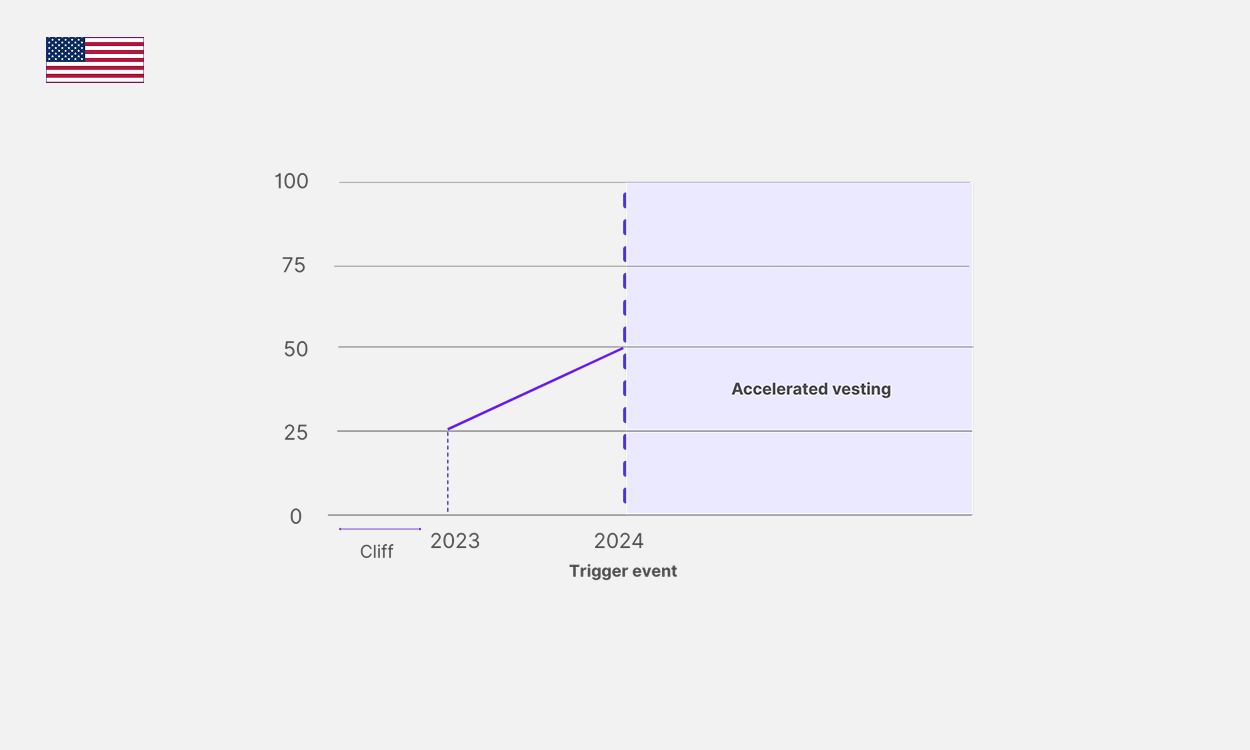

Vesting is the period during which employees gradually earn the right to exercise their stock options. It’s typically structured over 1–4 years, often with a one-year “cliff,” where no options vest until the end of the first year. After the cliff, vesting continues monthly or quarterly.

2. Exercise process

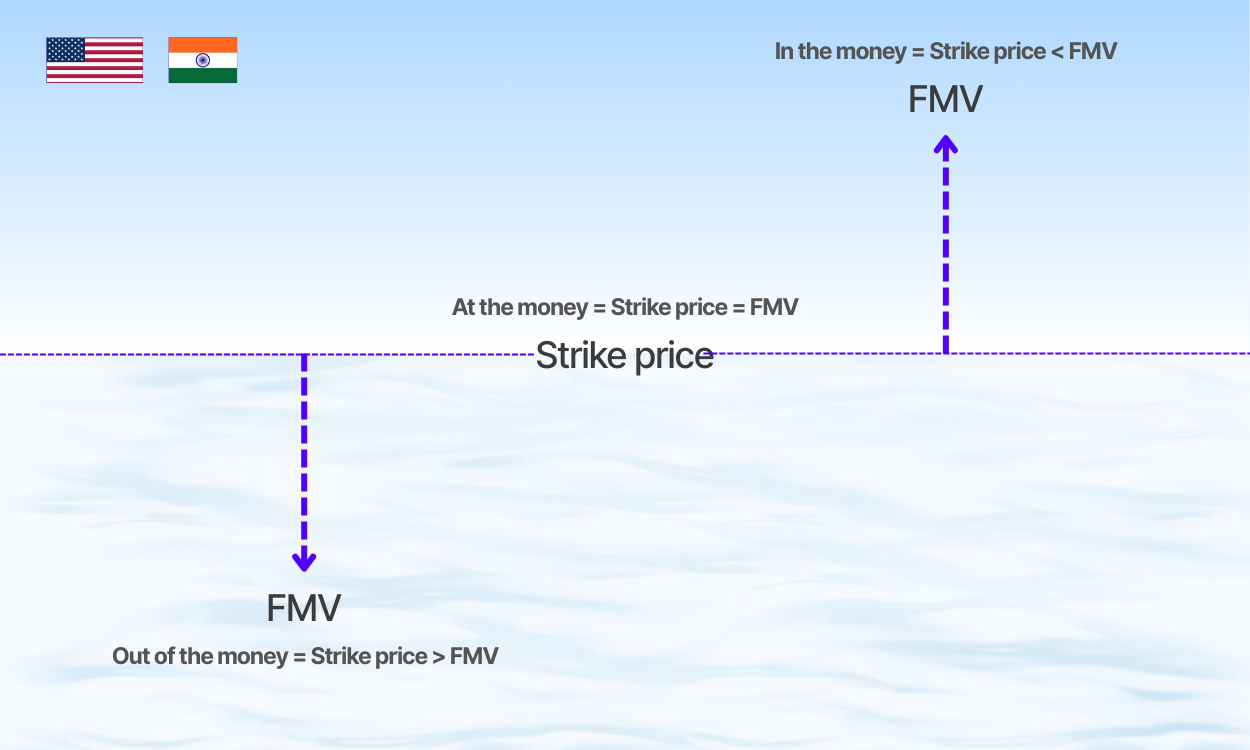

Once the options are vested, employees can exercise them by paying the pre-determined exercise price. This is when the financial and tax implications come into play. Under the Income Tax Act, perquisite taxation is triggered, calculated on the difference between the fair market value (FMV) of the shares on the exercise date and the exercise price.

3. Allotment of shares

Once the employee exercises their vested stock options, the company will allot the corresponding number of shares, typically by transferring them from the ESOP pool. A formal agreement or resolution is then executed, outlining the number of shares allotted, the exercise price paid, and any other pertinent terms.The company's shareholder register is updated to reflect the new ownership, and the employee receives share certificates, either digital or physical, as proof of their ownership in the company.

FAQs

1. Is ESOP a part of CTC?

Yes, ESOPs are generally considered a part of the Cost to Company (CTC).CTC typically includes fixed compensation (salary), variable components, and benefits, along with ESOPs. While ESOPs are part of the total compensation package, their value is realized only after they are vested and exercised.

2. Is ESOP better than salary?

Whether ESOPs are better than salary depends on individual preferences and the company’s growth prospects.While a salary provides immediate, guaranteed cash compensation, ESOPs offer the potential for significant future financial gain if the company performs well and its share value increases.

3. What happens to ESOP if I quit?

If you quit the company before your ESOPs fully vest, you typically lose the unvested portion of your options. For vested options, you may have a limited window to exercise them after your resignation.If you don’t exercise your options within the allowed period, they may expire.