.png)

Many startup founders unknowingly end up promising stock options or similar devices as a part of the compensation to their employees without having a formal ESOP scheme in place. Suppose you’re an Indian startup founder who hasn’t set up an options program yet but has already started promising options to the team. In that case, you may have unintentionally put some employees in a problem. Fortunately, it’s possible to mitigate some of the impacts of this, and we’ll detail how in this post.

A “Scheme document" is the document that records all the terms and conditions associated with the ESOPs offered to the employees, right from the total number of units being authorized by the company (known as the "Option Pool") to what happens to the vested units of an employee after they leave the company.

A private limited company can set up their ESOPs in India by referring to legislation such as the Companies Act, 2013 and rules made thereon. Here is a rough outline of what companies should do to form an options program formally:

- Draft an ESOP scheme. EquityList has in-house experts to help you set up and implement your scheme effectively.

- Get the ESOP scheme approved by the board of directors

- Then, shareholders must approve the ESOP scheme via a resolution at a general meeting.

- Then, your company secretary will handle the storage/filing of the resolutions as appropriate.

- Employees should be granted the stock options in a ‘Letter of Grant’ if approved. This will have all the written information about the alternatives, such a number of granted options, vesting schedule, exercise price, expiration date, etc

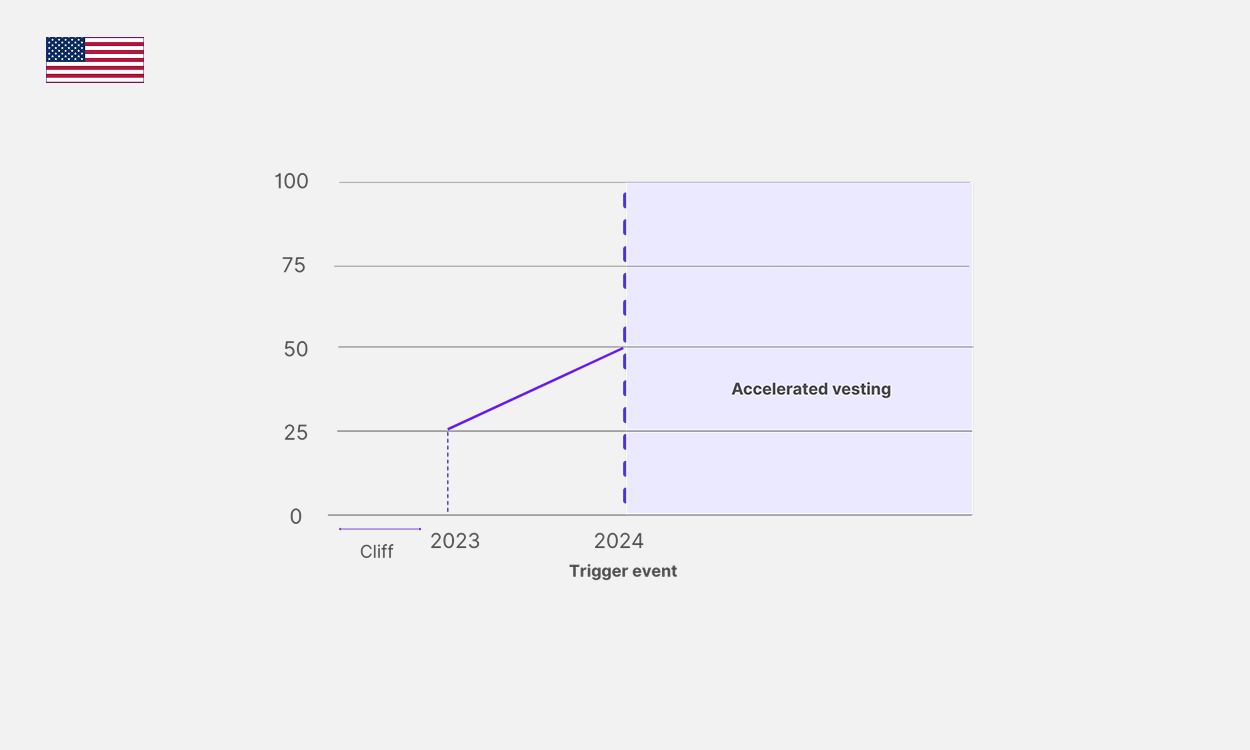

Unlike regulations in other countries like the US, the Indian Companies Act, 2013 requires every ESOP scheme to have at least a one-year cliff attached to it, for which the earliest start is when the ESOP scheme has been approved. At the end of the cliff, 25% of the offered options pool gets vested and the vesting schedule for the remaining options can happen monthly, quarterly, semi-annual or annually or it can be entirely custom based on company discretion as long as it is clearly stated in the scheme document.

For example, a company (SaaS Co) raised its seed funding in January 2020. Their founder Jaya, had hired her first employee, Rahul, six months ago. Let’s say Rahul’s starting date at SaaS Co is mentioned as 1st July 2019 on his confirmation letter, along with the details of the compensation structure offered to him, which is a combination of Rs. X as his annual cash compensation + Rs. Y worth of ESOPs.

However, when joining, Rahul wasn’t formally presented with ESOPs because the board approved no ESOP scheme. But Rahul believes that he has the confirmation of the ESOPs offered to him through the mention of it on the confirmation letter and was under the impression that Cliff will start on the date of his joining.

As part of the Seed Round, Jaya officially forms the ESOP scheme. She gets the board approval and files the regulatory paperwork on 1st Feb 2020. At this point, she can send the grant letters to all the employees whom ESOPs have been promised over time. The scheme that comes into action on Feb 1st states the terms and conditions defining the ESOP allotment to all employees.

Here's the catch, according to Indian laws neither the vesting period nor the grant date can begin before the ESOP scheme was formally approved. The mandatory one year cliff imposed by the Companies Act means that vesting for anybody can happen exactly one year after the scheme formation date, i.e. 1st February 2021 (considering the mandatory one-year cliff), considering that someone was promised ESOPs on the date of scheme formation, i.e. 1st February 2020. Now what happens to the employees who have been promised ESOPs before the scheme formation date?

One solution to such a situation is “compressing” the vesting schedule. This entails creating a one-time unique vesting schedule for each employee where instead of the standard 25% vesting at the end of the first year, the complete pending percentage that the employee would have had gets vested at the end of the cliff and the remaining pool of offered ESOPs get vested as per the grant details, i.e. monthly, quarterly or annually. This ends up compressing the complete vesting schedule by some time but ensures that the employees get what they have been promised within the time frame that they should have as promised earlier.

In our case, 100% vesting is supposed to happen monthly over 4 years, with a mandatory cliff of one year with 25% of the entire pool vesting at the end of the first year and then in equal increments monthly after that.

Let’s say Rahul was offered 480 units on his date of joining, and the original start of the vesting period was supposed to be 1st July 2019, however, now vesting for anybody can only start from 1st February 2020. If we follow the new schedule, Rahul loses 7 months of vested ESOPs that he would’ve gotten in an ideal scenario. In a compressed vesting schedule, on his first vesting event (i.e. on 1st February 2021), Rahul will have 190 vested options instead of 120 (according to the 25% math). Here is an abbreviated version of the vesting schedule as promised, and under vesting compression.

To help you understand this better, we can provide you with a more detailed spreadsheet explaining how this “vesting compression” works.

Since this is a problem many of our customers face, the EquityList platform can automatically solve “vesting compression” for you by creating unique vesting schedules for each employee based on when they were promised ESOPs and when the scheme was formed. Our software creates a single grant with a unique vesting schedule to allow the employee to benefit from their originally promised terms while staying compliant with regulations on vesting.

Pitfalls

There can be multiple other problems that can arise in such scenarios where compressing the vesting schedule may not solve all your problems. For example, what happens if an employee was promised units that would have been vested had the scheme been formed earlier but left before the one-year cliff date post the scheme formation. In this case, per ESOP regulations they will not be entitled to any vested units.

According to our example, if Rahul ends up leaving the company on 1st September 2020. He should ideally have 150 vested options until then (considering he was promised ESOPs on 1st July’19) but because of this delay in formation (scheme got created on 1st Feb’20 so no vesting could be considered before that), he technically hasn’t even completed his cliff by then.

In such scenarios, we always recommend our customers to seek professional legal guidance and try to find solutions so that the employees do not end up short-changed. We have had a few of our customers & advisors come up with workarounds and are happy to share those with you if you are in this position. In order for employees to value ESOP grants, it's important to offer fair terms and get your paperwork in order.

What can employees do to avoid such a situation?

- Ask about the terms of the ESOP scheme at the time the offer is being made.

- Check if they have a scheme in place already, inform them of the possible difficulties that they may have to face if they don’t have one.

- Ask about the expiration & exercise terms.

- Proactively ask for a grant letter with a laid-out vesting schedule

What can founders do to avoid such a situation?

- Most scheme documents allow the board to alter the vesting schedule on a grant by grant basis as per their discretion. Check if your scheme allows you flexibility to help you manage the situation.

- Seek legal advice timely with regard to your ESOP policies.

- Communicate the situation to the employees and ensure that this can be solved.

Start using EquityList:

- We help you digitize and validate your ESOP schemes, grants, and cap tables early in your startup journey so that you don’t have to end up facing one of these situations.

- We help you solve most of the problems that you may face:

- Free ESOP scheme document bundles

- Automatic grant letter generation and e-sign facility

- Compressing vesting schedules for “backdating” ESOP grants

- In addition, we connect our customers with the best in the industry to help them take care of matters that we can’t directly resolve.

For any questions, reach out to us at help@equitylist.co!